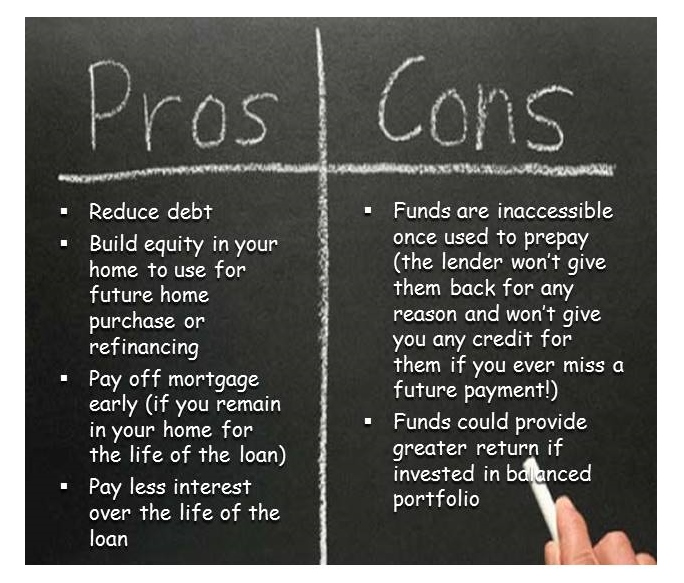

Clients occasionally raise with us the question of whether to make prepayments against the principal on their mortgage. Unfortunately, we do not have a one-size-fits-all answer to this question. Below are some pros and cons and a discussion of factors to consider in determining whether to prepay on your mortgage.

Alternative Use of Funds: The most significant consideration is to what use you would otherwise put the money. If, for example, you are considering prepaying a modest amount (e.g., rounding up your mortgage payment to the next hundred) that you would otherwise use on clothes or eating out, then prepaying would allow you to build a bit more equity in your home while decreasing your monthly personal expenses (a double bonus for any financial plan!). If, however, you are considering prepaying a more substantial monthly amount that you would otherwise save and invest, then you might be better off investing.

If faced with this enviable problem of extra money at the end of each month, consider first whether you have an adequate emergency fund, whether you are maxing out your retirement plan contributions, whether you need or want to build a taxable investment portfolio, and, if you have young children, whether you are saving for college expenses. If the answer to any of those questions is “no,” start there. If you feel comfortable about your savings toward each of those goals, you might still be better off investing extra cash flow in a non-retirement investment account, which would have potentially a better return and certainly more liquidity than prepaying your mortgage.

Interest Rate vs. Expected Returns: One advantage of prepaying your mortgage is that you will pay less interest on the loan over time. However, with current interest rates near historic lows, mortgage rates are considerably lower than the expected long-term return from investing in a balanced portfolio. For example, an investor might expect annual returns of approximately 7 to 8 percent from a 60-40 portfolio (60% in equity, 40% in bonds) over the long term but pay only 3 to 4 percent interest on a 30-year fixed mortgage.

Also, consider the after-tax value of paying interest on your mortgage. If you itemize deductions, you at least “get credit” for the mortgage interest that you pay, since you can deduct that amount from your taxable income. If you take the standard deduction, however, that may make it more appealing to try to pay off your mortgage faster.

Personal Profile: An individual’s attitude toward debt and stage in life can also be a significant factor in the prepayment decision. Certain individuals are extremely debt-averse and would be much happier without a mortgage. Others are approaching retirement and would appreciate the simplicity and security of having their mortgage paid off before ceasing work, especially if they are going to remain in their homes for the foreseeable future and will not receive a pension. If, however, you are not particularly averse to debt or you are planning to move (and therefore obtain a new mortgage anyway) in the near term, then making prepayments might hold less appeal.

If you have questions about whether pre-paying the mortgage is right for you, please feel free to call or email any time.

If you have any questions about your financial future, we're here to help. Please use this form or feel free to call or e-mail us.

(703) 385-0870